States are Playing Moneyball Through Pay for Success

Outside of the nation’s capital, governors are also playing Moneyball. A growing number of governors from both parties are eschewing partisanship to solve long-standing social problems while limiting taxpayer risk. They are using a new funding tool called “Pay for Success,” also known as “Social Impact Bonds,” in which the government reimburses private partners only after the private actors achieve success in tackling a social challenge.

“Pay for Success” is a pathway from the blind, across-the-board spending cuts that are commonplace in Washington, to the smart, innovative spending choices that communities across the country need to solve long-term problems.

So, how does it work?

“We’re constantly looking for new ways to innovate in order to provide better value for taxpayers, and the social impact bond model can help us do that. Not only does this approach help pursue solutions to tough problems, but it does so in an accountable, results-oriented way.” – Gov. John Kasich, R-OH, June 2013.

It starts with government identifying a goal such as reducing prison recidivism, reducing homelessness, boosting employment or improving job retention. Next, the government contracts with private investors who raise capital for a project designed to achieve that goal, and with a nonprofit or other provider to deliver results. The programs undergo rigorous evaluations to determine if the desired outcomes have been achieved. Only after success is determined does government spend any money. If the project fails, taxpayers don’t spend a dime. This limits taxpayer risk and incentivizes success.

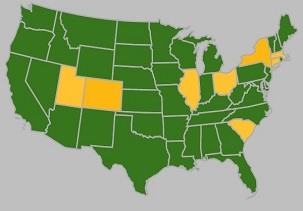

Programs are taking root in Colorado, Connecticut, Illinois, Massachusetts, New York, Ohio, South Carolina and Utah with more on their way. The Federal government also has created Pay for Success programs to assist governments at all levels as they tackle challenges that have plagued communities for far too long.